Solving search, trust, and friction

Two‑sided marketplaces matches supply (providers) with demand (buyers) and monetizes the match, usually via a take rate (a % of GMV), per‑transaction fee, or a subscription to access the network. Marketplaces solve search, trust, and logistics frictions; the resulting liquidity (speed + probability of a successful match) creates network effects that can become a moat.

There are same-side and cross-side network effects, which each may be positive (e.g. more sellers on Amazon begets more buyers) or negative (e.g. sellers compete with other sellers).

It requires focus to decide which parties to prioritize in what order amongst suppliers, buyers, and often other stakeholders, especially before the network has achieved escape velocity. Because both sides have networks effects in and of themselves that reinforce each other, 2-sided marketplaces have far higher barriers to entry than 1-sided (which are more about monetizing customer loyalty).

Even two-sided markets with strong positive network effects may not have winner-take-all dynamics and be optimally supplied by a single platform at mature scale if the market doesn’t have high multi-homing / switching costs, similar needs amongst all consumers or practically indefinite returns to scale.

Marketplace vs. Platform vs. Aggregator:

Platforms enable transactions (APIs, tooling) and are often essential to make products work; value accrues by facilitating the relationship. Aggregators specifically aggregate demand, often commoditizing suppliers. The network is “internalized.” Platforms tend to support supplier differentiation; aggregators often compress it.

Pros

Cons

When the model fits

Use a two‑sided marketplace when all are true:

Mechanics of the model

Pricing

Multi-sided generally networks shouldn’t price via traditional rationale (i.e. marginal cost for competitive industries and WTP for those with high barriers as seen in the top graph). Instead, they must take into account network effects and the particulars of each side in their pricing strategy, often resulting in a subsidy for one side.

Note that one must of course be careful with subsidization, especially if the good has meaningful marginal costs (most physical goods) or if you paying side can avoid paying for your services (e.g. Netscape subsidized its browser to individuals but web site operators didn’t have to buy their servers).

Each cohort-year, more revenue than the year prior, except for the COVID cohort (2020) (not surprising - many that year were forced in). More impressively, all other cohorts held on to COVID bumps -- eg., 2017 cohort in years 3-5 was 1.74x, 3.0x, *3.2x* of year 1 GTV. The bump stuck!

So while $CART is B2C, it has the revenue durability of a so-so SaaS company. $CART beat us over the head with this superannuity point later on with this figure:

Instacart+ is an impressive driver of growth and durability

It is astounding how big the subscription program is. 57% of $CART's revenue comes from subscribers. 5.1M members in Q2 2023, vs 7.7M monthly actives then.

This is a very strong return on investment. And if DoorDash can continue holding onto and monetizing these customers in future years, those PAV estimates continue to go up and up.

That said, I would be remiss if I did not mention that the absolute dollar amount of this return is not all that large. A five-year CLV of $54 is not a whole lot of value in an absolute sense. This is primarily due to the very thin margin profile of the firm. What sort of overall corporate valuation does this imply? To justify a valuation of $25-30B+ when a lot of the core market has already been acquired, it would seem like we may need to see something more -- a transformative new vertical, or a way to dramatically expand TAM.

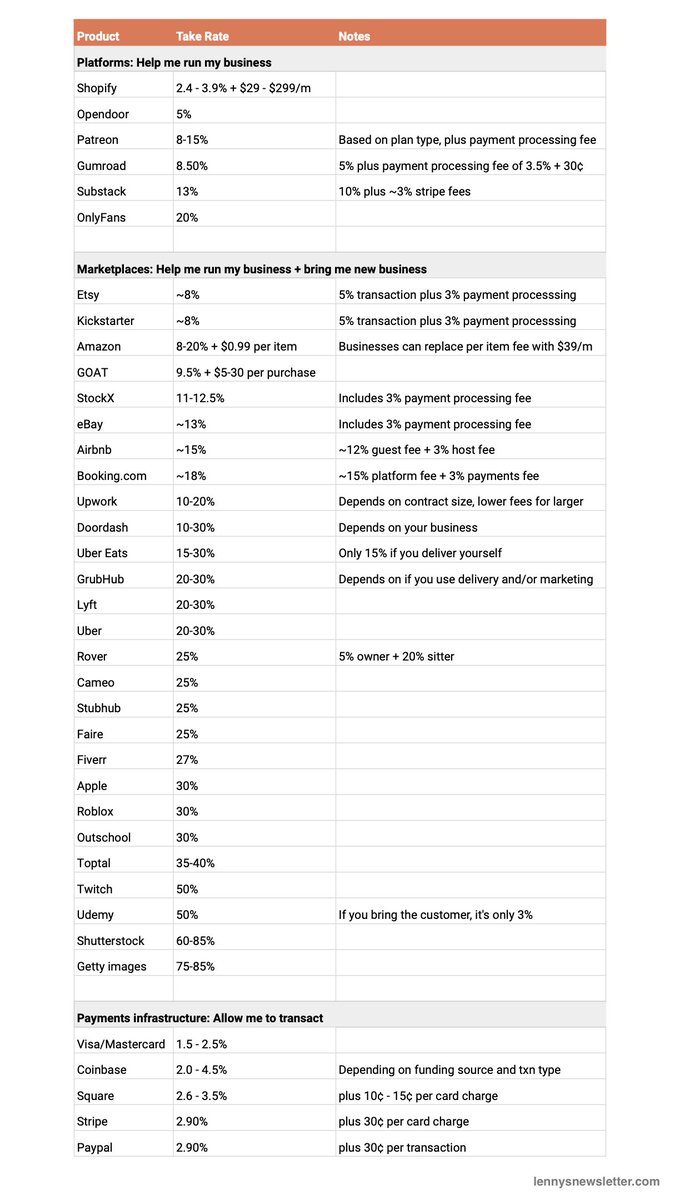

DoorDash: great unit economics, but many unanswered questionsTakeaway #1: There is a relatively clear distinction between “platform” businesses taking 5-15% (which make it easier for you to run your business, e.g. @Patreon @SubstackInc), and Marketplaces taking 10-50% (which bring you new business as well, e.g. @DoorDash @BookCameo)

Takeaway #2: Differences in take rates are primarily driven by three factors: (1) whether you can drive new demand, (2) how much convenience you provide the seller, and (3) the level of competition in the market.Take rate = Convenience + Demand - Competition

3/ For example: Gumroad (8.50%): High convenience + Little demand gen - Medium competition Substack (~13%): Very high convenience + Little demand gen - Medium competition Twitch (50%): Very high convenience + Very high demand gen - Very low competition

4/ Surprises:1. @OnlyFans (a platform that doesn’t bring any demand) is able to charge 20% (a rate normally reserved for marketplaces). This is because they solve a major pain point for their creators (e.g. accepting payment for sex work) and there isn’t much competition.

2. @Etsy's fees are at the low end of the spectrum for a marketplace (i.e. even lower than Substack, which doesn’t drive demand). This is probably because of heavy competition with Amazon.

3. @toptal is able to charge close to 40% as a labor marketplace. This is likely due to how much time and effort the platform saves both supply and demand.

4. @Twitch takes 50%. This likely speaks to the quality of the product and the significant network effects.5. @Shutterstock and @GettyImages take up to 85%. This is likely due to how little work there is to get paid once you’ve uploaded your photos.

Lenny Rachitsky (@lennysan) on Xthat amazon number is way too low. if you don't go with FBA the shipping requirements are so high it's very hard to get prime. no prime shipping = sales tank. so realistically FBA is more like 25-30% when you put in all the fees. not counting advertising which is another 8-10%

Audible takes 60-75% commission on each audiobook sale

(60% if you sign a multi-year exclusive deal with them, 75% otherwise.)

YouTube: 45% (ads) Instagram takes 100% (of revenue from ads they sell; no automatic share with top creators)

Stat from Instacart that highlights the moat these ZIRP-era companies have: “It took us 100 million orders before we were able to get to positive unit economics”