Partner with incumbents for scale up, own the royalties

High tech, discovery-focused startup develops novel good often to PoC level and then partners with incumbent that has mature, scaled distribution / manufacturing capacity, often earning an upfront payment and downstream royalties on sales

Gingko Bioworks, Mattiq, VS Particle, Genomatica

Compound portfolio company Orbital Materials

Startups focused on discovering novel products in materials science, syn-bio, chemicals, cleantech, etc. often partner with incumbents on scale-up, at least of the first product(s) discovered. It allows startups to quickly generate revenue off a large amount of R&D that’s still years away from scaled revenue. It also absolves them of raising $100Ms to $1B of maximally dilutive VC funding to build a relatively low margin manufacturing plant.

The dynamic exists because the technical scale up from lab-bench quantities to profitable manufacturing to scaled distribution are collectively at least as difficult and time consuming as the discovery/invention phase. They also require distinct core competencies from discovery.

The JV model is particularly relevant for startups for whom a core competency is generating novel materials and that plan on developing multiple. And, it can make even more sense for products with razor thin margins.

On the other hand, it may not make sense for startups commercializing one product or a few tightly highly related ones, that can go after high value products initially with a small-scale plant, and whose medium- to long-term core competency needs to be in production efficiency. For this, think of Solugen. This route may be meaningfully harder in the non-ZIRP era.

The startups’ goal is generally to own as much as of the value chain as possible. The degree to which it can do that depends largely on the incumbent (though also on whether the startup can technically deliver in a short timeframe). Less technologically sophisticated customers for whom R&D is far from a core competency generally accept a more finished product that it can drop into existing processes. Whereas, more sophisticated players may just want initial hits or PoCs that they will then optimize internally.

The contract terms can be challenging depending on the area, as I discussed in my post on materials science:

The contract terms aren’t exactly easy either. The incumbent may be concerned about even defining the problem to solve, as that’s viewed as IP. Then, there’s debates about who owns the data. Most important of all is payment structure. In the pursuit of climbing up the value chain as high as possible, the best case is generally an 8-figure JV with phased payments ultimately resulting in a PoC that the incumbent then scales with their manufacturing / distribution base and ideally pays some ongoing royalty for.

Likewise, Gingko has struggled mightily to retain much of the value it creates for its customers. For those in industrials, it no longer gets equity/milestones/royalties on the products its service helps develop. And broadly, it no longer gets to keep any of the data it generates on behalf of customers, cutting off its long-term pitch of having a data flywheel. Gingko also had the rather unique problem for this business model of serving startups, who’d often pay in their own equity (almost all of which got wiped out).

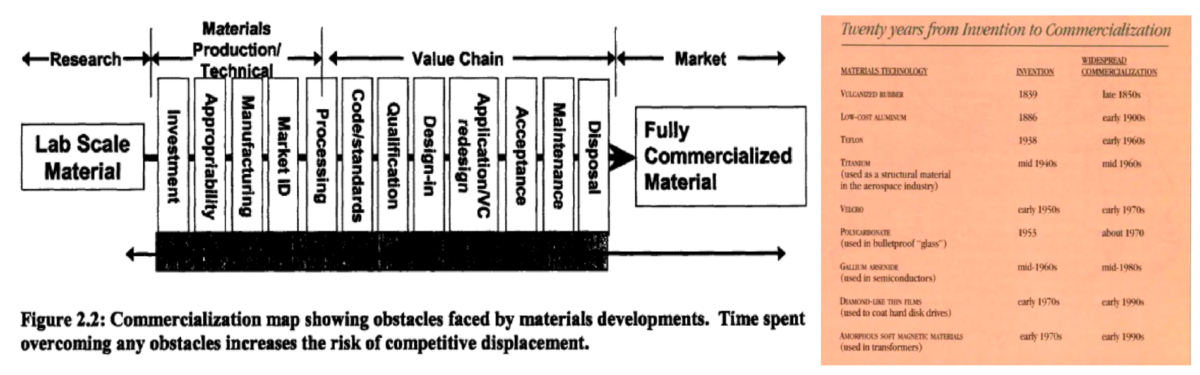

For more historical color on the commercial path to bringing a novel material to market, see these three resources. They broadly stress the importance of thinking harder than materials scientists are used to very early on about the minute details of its commercial integration, minimizing the complexity of value chain integration (drop in, modular, etc.), and leaning into smaller, fast growing markets uniquely enabled by the new technology as opposed to first starting with the largest, homogeneous ones.

Economics Mechanics

Royalty ranges (only as ball-park reference points):

BE Summit 2024 | 12 Keys to Scaling Up: Unlocking Cleantech Commercialization

IP Valuation Manual:

Cdip 17 Inf 4 Val Man BbBest practices for preparing for successful technology licensing:

Wipo Pub 903The Structure of Licensing Contracts

Licensingcontracts Cd733012 83e0 44a7 Bdfc 802f0281aad9